Getting America Back to Work

All of the growth and flow of money made little difference to the quarter of the population out of the loop. Roosevelt’s second challenge, after stabilizing the economy, was to get the droves of unemployed doing something productive. A wave of construction projects washed across America, providing work to those who needed it. Small farmers were organized into collectives and taught that flooding the market with crops actually made them less money. Businesses were forced to keep wages stable, boosting up those who were still employed, and providing new openings for those who were not. Strict labor laws developed what we would recognize as a modern work week. Older workers were nudged out of the labor market to make room for the younger generation. Social Security soon provided retirees with an income beyond their laboring years.

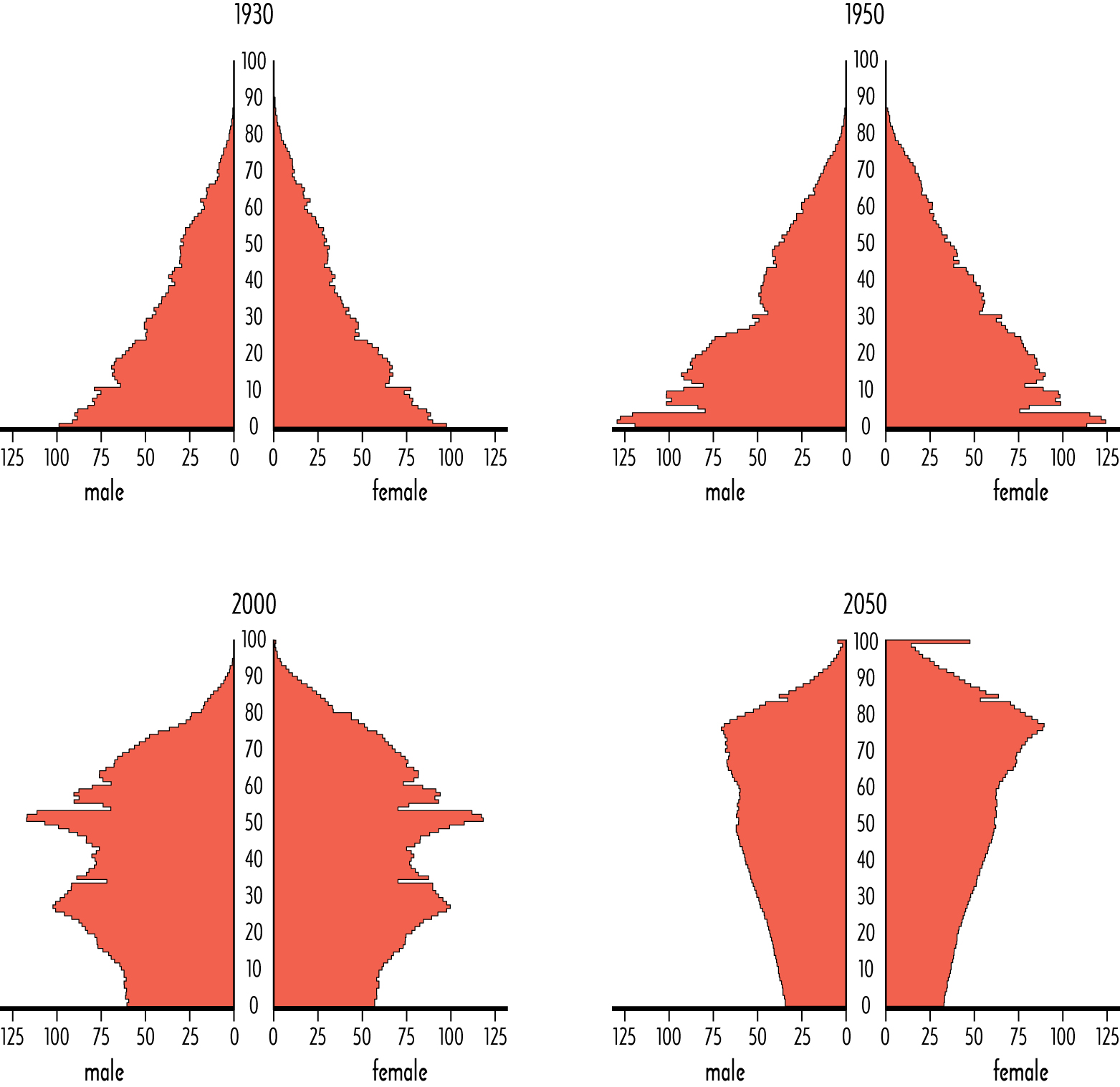

This last point is the one I wish to discuss. During the first half of the 20th century the United States still possessed vast tracts of untapped land, immense natural resource reserves, and had room for a continual influx of immigrants and rapidly growing population. The Social Security system was established with all of these aspects counted into its equations. Most importantly it relies on having many young workers providing for few old retirees. It sets up a requirement of unlimited growth.

Above is a representation of overall population by age. Age is represented in the center; the length of the bars stands for how many people of that age. We are looking at overall trends, so exact population values are not important to this example. You can see the baby boom generation appear in the 1950s, and see the Echo Boomers, Generation Y, establish themselves in the workforce in the 2000s. Notice how the population pyramid has changed shape. Modern medicine has extended lives, and the overall modern environment has reduced population growth rates. Keep following these trends into the future and the survivability of Social Security comes into question. Now consider this quote:

"We put those payroll contributions there so as to give the contributors a legal, moral, and political right to collect their pensions and unemployment benefits. With those taxes in there, no damn politician can ever scrap my social security program." -Franklin Delano Roosevelt

Absent an ever expanding working population, through immigration or offspring, Social Security must be reworked. Benefits will have to be reduced, and age requirements must be increased. Nevertheless, as Roosevelt keenly stated, no politician will ever advocate such drastic changes and have any hope of ever being elected again.

The American Dream

Owning one’s own home has long been seen as a large step toward achieving the American Dream. Outright ownership allows you to be free of a landlord and live mostly as you wish. The sense of freedom that comes with homeownership is undeniable. The New Deal saw the creation of generous loan programs developed to help families purchase their own home. More homeowners led to more property tax collected by the federal and state governments. It was seen as a win-win situation.

The dark side of the new arrangement saw what was once a family’s greatest asset become their greatest liability. Historically loans on single family homes required close to a 50% down payment, the remainder being paid over a term of 3 to 5 years. The stiff financial requirement saw that only about 45% of Americans were homeowners.

Enter the FHA, created in 1934 the Federal Housing Administration substantially eased the monetary demands of homeownership. Upfront costs were greatly reduced and loan terms stretched to their now familiar 30 years. The program saw vastly expanded activity and further reduced costs to buyers after the end of WWII. Its effects to date have increased the homeownership rate to just shy of 70%.

Making homes affordable has inexorably tied Americans to their mortgages. Affordable housing nudged us over the slippery slope of living beyond our means. Needing transportation to jobs in the city, Americans purchased automobiles in record numbers. They also filled their new houses with an ever growing supply of appliances and gadgets. The practice of “Keeping up with the Joneses” was driven to all new heights. More and more frequently purchases of status symbols were done so on credit. Empty space in Americans’ homes became a debt engine of incomparable magnitude.

Where are We Now?

We have stayed on our course of growth and expansion, but are testing the limits of our current technology to keep up with the rates. Gold and silver have been abandoned as backings for our currency. Instead our money is backed by loans taken out by the government from Federal Reserve Banks (more on this interesting arrangement later). Within twenty years we will face a sea change of policy relating to retirement. If we continue to wait until the problem confronts us it will be too late to address it. The recent shock to the housing market has shown us the dark side of living with so much debt. Our recovery this time around will be markedly slower than in the past.

My advice is as follows. Strive to keep debt down to clearly manageable levels if not eliminating it entirely. It can be a powerful tool when used for worthy causes such as education, recovering from an emergency, and business expansion. However, be wary of its long term consequences when liberally used for other purposes. If you don’t want to be doing what you are now for the rest of your life, then prepare yourself financially for when you change direction. Expand your financial literacy; learn about the relationships between money, risk, and time.

No comments:

Post a Comment